Braze - The Better Way for Brands to Engage with Their Customers

Will this customer engagement platform engage with your portfolio?

Brief Overview

Braze is a customer engagement platform used by businesses for multichannel marketing. The company went public at $65 per share and closed at $91. Braze is attempting to disrupt the marketing industry by taking on industry giants like Adobe and Salesforce. Read more below to learn about the company.

Basic Company Info

Name - Braze

Year Founded - 2011

Ticker Symbol - (NASDAQ: BRZE)

Website - https://www.braze.com/

Headquarters - New York, New York

Number of employees - 1000+

Sector - Technology

Industry - Software - Application

Market Cap (11/18/2021) - $7.6 billion

IPO Date - 11/17/2021

What does Braze Do?

Founded in 2011, Braze bills itself as a:

…leading comprehensive customer engagement platform that powers customer-centric interactions between consumers and brands.

What exactly does customer engagement mean? Braze states:

…customer engagement is anything your company’s customer-facing teams are doing that supports a direct connection with your customers.

Braze offers a vertically integrated approach for brands to connect customers via in-product channels like mobile app messaging and out-of-product channels like text messaging or Facebook ads. Additionally the company provides reporting and analytics capabilities that enable brands to derive actionable insights. According to founder and CEO William Magnuson, Braze was founded with the belief that mobile adoption would change business and society. The goal was to build a company using new technology that brands would trust with its most important asset - their customer relationships.

Braze emphasizes that its technology helps brands connect in a way that is more human and personal.

What Problem is Braze Solving?

Braze is disrupting legacy marketing and customer engagement technologies. Legacy companies suffer from many limitations such as:

Initially architectured as single-channel point solutions - such as email marketing platforms. Legacy companies make bolt-on acquisitions to address the gaps but this results in siloed architectures and feature sets

High latency - Batch processing technology in legacy marketing clouds results in data processing at fixed intervals and not in real time. Brands require real-time data processing

Time-consuming and difficult to implement - Legacy cloud companies are inherenty inflexible and expensive to customize. This leads to longer implementation times

How Does the Business Model Work?

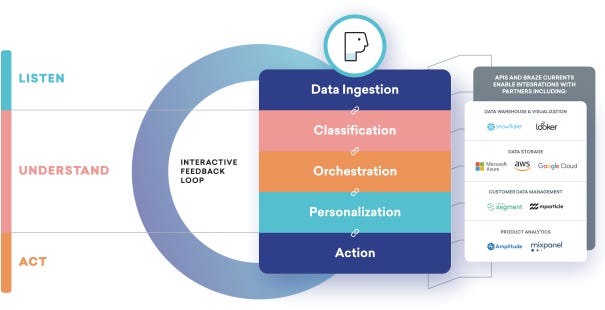

Braze claims that their vertically integrated platform helps brands to perform three core functions: “listen”, “understand” and “act”. More specifically the framework operates as follows:

Listen - Listen to the customers

Understand - Understand customers more deeply

Act - Act on the understanding in a human and personal way

According to the company, the secret sauce behind the “listen”, “understand” and “act” framework is several functional layers that are unified by an interactive feedback loop of continuously flowing data. These five layers are as follows:

Data Ingestion - brands integrate software directly into their consumer interfaces such as website or mobile app and data flows automatically into Braze’s platform

Classification - the platform classifies each consumer based on demographics, past behaviors and current actions

Orchestration - brands deliver contextually relevant messages to engage with consumers

Personalization - brands customize their messaging based on information already gathered

Action - execute marketing stratgies that are focused and relevant

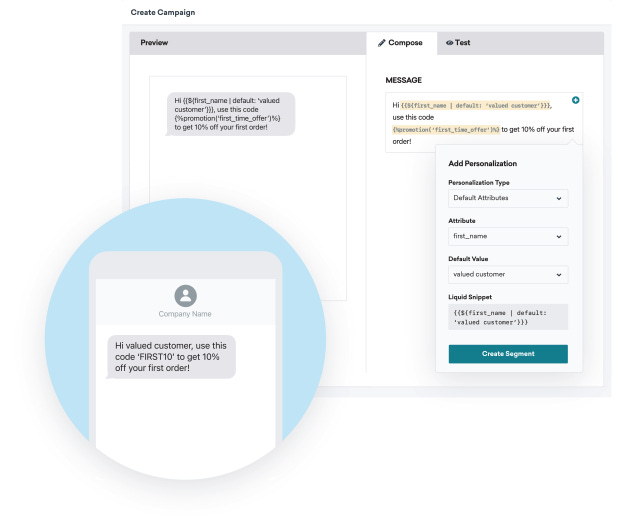

The “Understand” framework plays the really important part. After digesting the data, Braze uses machine learning to to segment customers into different groups using real-time data. Braze is able to analyze these segments of customers and see how they perform relative to certain KPIs. For instance Braze can identify potentially high risk customers, i.e. those that are likely to churn, and this allows brands to try and discourage them from leaving. After customers have been segmented, campaigns can be created and personalized messages can be sent out such as this one below:

Braze claims that there are 3 billion+ monthly active users that send 1 trillion messages with brands that are powered by their platform.

Competitive Advantages

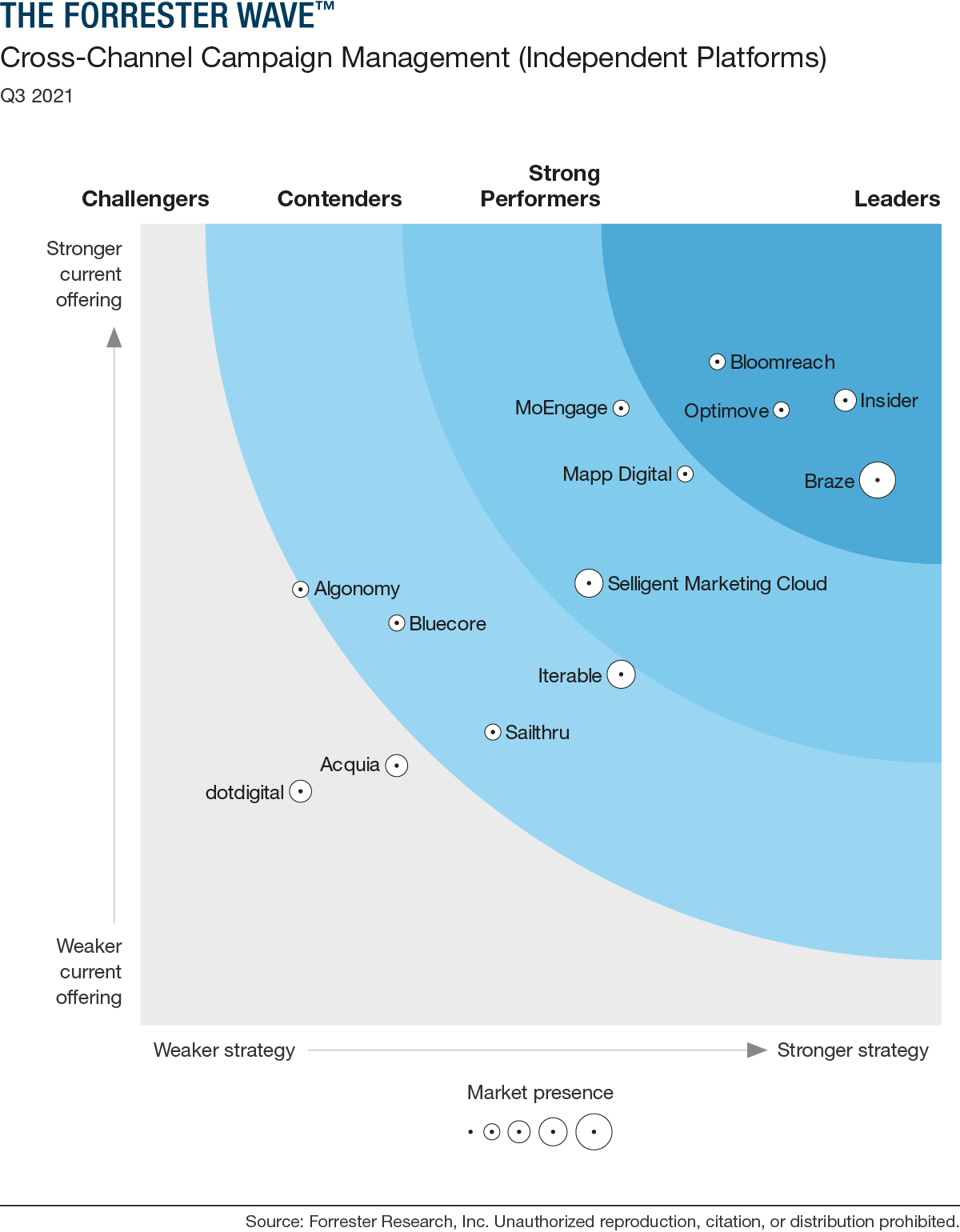

Because brands connect to Braze’s platform directly, Braze offers brands a way to interact with their customers using first-party data. Additionally, Braze’s platform support interactions across multiple-platforms both in-product (within the brand’s own properties such as mobile app) and out-of-product (text messages, Facebook, Google, CTV etc.) all while orchestrating real-time personalized messaging experiences. The company’s integrated technology stack allows brands of all sizes to scale rapidly and securely. Braze also supports direction integrations with many popular cloud data service providers such as Snowflake, customer data management platforms such as Segment and analytic solutions companies such as Amplitude. As a result, Forrester named Braze as a Leader in their “Cross Channel Capaign Management (Independent Platforms)” Q3 2021 report:

Leadership

Two of the three founders of the company are still with Braze today. The story of Braze began when CEO Bill Magnuson and CTO Jonathan Hyman participated in and won TechCrunch Hackthon in 2011. The other co-founder, Mark Ghermezian, an entrepreneur and investor, is not with the company any longer (an interesting side note - the Ghermezian family is known for building the 3 largest shopping malls in North America including the Mall of America).

Not only is it impressive to be the co-founder and CEO of a company that is now worth $7.6 billion (as of 11/18/2021), but Bill Magnuson is only 34 years of age. Magnuson graudated from MIT in 2009 with a degree in Computer Science and minor in Economics. His only professional experience prior to starting Braze was being a software engineer for 1 1/2 years at Bridgewater Associates and an intern at Google. Magnuson owns 3,729,499 shares, or 4.4% of the company, making his current ownership in the company worth just over $300 million at today’s prices.

Jonathan Hyman, one of the other co-founders is also young at only 35 years in age. Hyman graduated from Harvard in 2008 with a degree in Computer Science. Hyman also worked at Bridgewater Associates for just under 3 years before co-founding Braze.

It is great to see that 2 of the 3 co-founders, with strong backgrounds in technology, remain in senior management positions at the company. Altogether, the directors and executive officers, as a group, own ~34% of the company. Interestingly, according to the S-1, none of the directors or executive officers are selling their shares. This should help ensure that the interests of shareholders are aligned with this group.

Leadership also scores very favorably on Glassdoor.com. Braze gets 4.5 out of 5 stars and CEO Magnuson receives a 97% approval rating. Braze is also consistenly awarded as a great place to work, including being being ranked #13 in Crain’s 2021 Best Places to Work in New York City for the third year in a row.

Client Base

Braze has built an impressive client that includes names like Paypal (Venmo), Etsy, FanDuel and GoFundMe. Other names not shown in the image above include HBO Max, IBM, Nascar and Sephora.

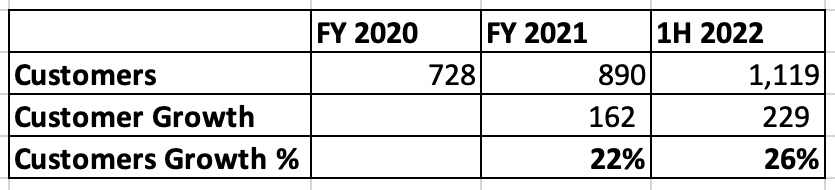

Braze has over 1,000 customers as of 7/31/2021. Interestingly, Braze added more customers in the first half of 2022 than they did in all of FY 2021. The absolute number of customers and growth rate in customers are both accelerating. This is certainly a positive sign:

Competition

Braze has some stiff competition but makes it clear in their S-1 that they believe to be the leader in the field. From the S-1:

There are several established and emerging competitors that address specific aspects of customer engagement, but we believe that none of our competitors currently offer comparable comprehensive customer engagement solutions.

Braze idenitifes competitors Adobe and Salesforce as “legacy marketing clouds.” Adobe and Salesforce are some of the earliest and most successful cloud companies. Both these companies built their marketing product portfolio through a series of acquisitions. This blog post from ActionIQ, a company that appears to be a competitor Braze (although not directly mentioned by Braze) states that:

Adobe and Salesforce’s expertise is not in customer data. Their pedigree is in content (think Adobe products like Photoshop) and business applications (think Sales Cloud)…Both “built” their marketing product portfolio (Cloud) through a multitude of channel-focused acquisitions…

Also not mentioned in the S-1 also is Hubspot, a publicly traded company that started as an inbound marketing software and added other platform features including a CRM suite and customer engagement suite. All of its Hubspot’s products were was built in-house on one code base.

Lastly Braze also identifies point solutions like Airship and MailChimp as competitors. These point solutions focus on one core area, such as MailChimp, a company that does email marketing and was just acquired by Intuit for $12 billion.

Growth Strategy & Financials

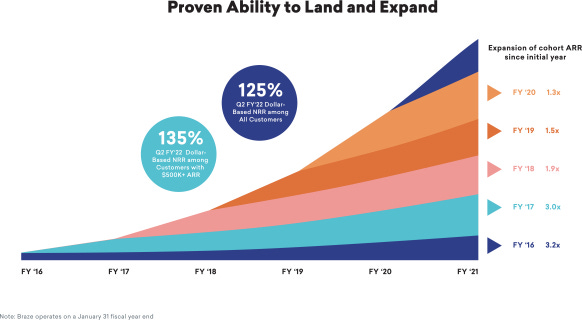

Braze employs the “land and expand” business model to grow the business. The company provides a great chart in their S-1 showing the increase in spend by each cohort based on their onboarding year. As shown below, customers onboarded in FY 2016 have increased their ARR, or annual recurring revenue, 3.2x as of FY 2021.

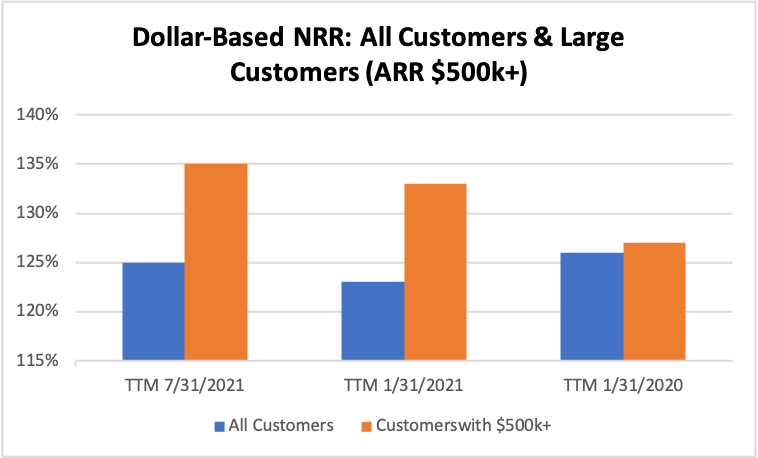

The Dollar-Based Net Retention Rate (DBNRR) among all customers and Braze’s largest customers, as defined by $500k+ ARR, has consistently been above 120% . The DBNRR for the largest customers is higher than DBNRR for all customers. This should be viewed favorably because enterprise customers tend to be higher quality and have less churn:

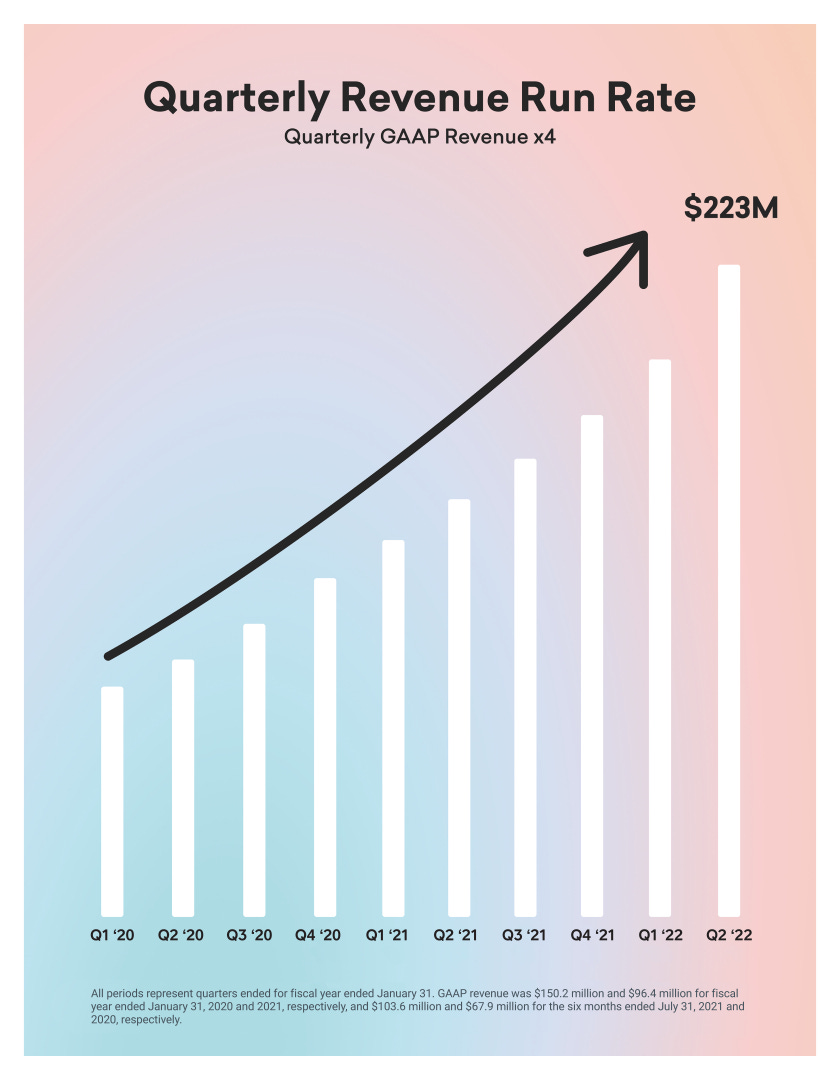

Revenue growth has been equallly impressive with sequential increases QoQ between Q1 ‘20 and Q2 ‘22. The company’s annualized revenue run rate, based on the quarter ending July 31, 2021 is $223 million:

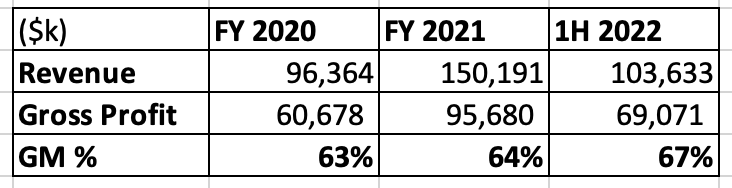

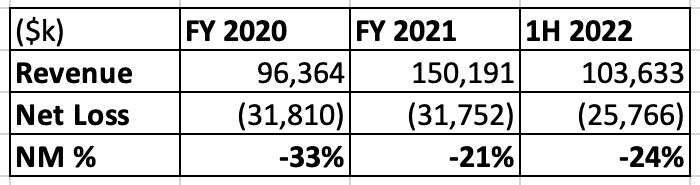

Revenue were up 53% in the quarter ending July 31, 2021 and 93% of the revenues (note that Braze’s fiscal year ends in January) were subscription, meaning that the company has $200 million in annual recurring revenue or ARR. Given the high % of subscription revenue, I hope to eventually see gross margins in the 70’s similar to top tier SaaS companies like DataDog and Zscaler. Gross margins for Braze has been in the mid 60’s but is trending in the right direction. Gross profit margin was 67% in 1H 2022:

Braze is not profitable yet. Net profit margin improved markedly with a 1,200 basis point increase in FY 2021 compared to FY 2021, however the trend has slightly reversed in the first two quarters of 2022:

Free cash flow has hovered right around the ($10m) range in FY 2020, FY 2021 and 1H 2022. FCF margin improved in FY 2021 but the trend reverted back in 1H 2021.

In terms of cash on the balance sheet, the company IPO’d on 11/17/2021 and raised $435.5 million in gross proceeds. All convertible shares were converted into common equity per the S-1 form. The company issued 90.3 million total shares consisting of class A shares and class B shares. They also granted underwriters a 30-day option to purchase 800,000 additional shares. Class B stock carries 10 votes vs. one vote for Class A shares.

Conclusion & Valuation

Braze’s consecutive sequential QoQ increases in revenue growth between Q1 ‘20 and Q2 ‘22 is impressive. Not many companies can make this claim. For a company with only $223 million in annualized run rate revenues and still early in the growth stage, Braze seems to be executing well. The company also continues to grow customers at a rapid clip, having added more customers in 1H 2022 than in the entire FY 2021.

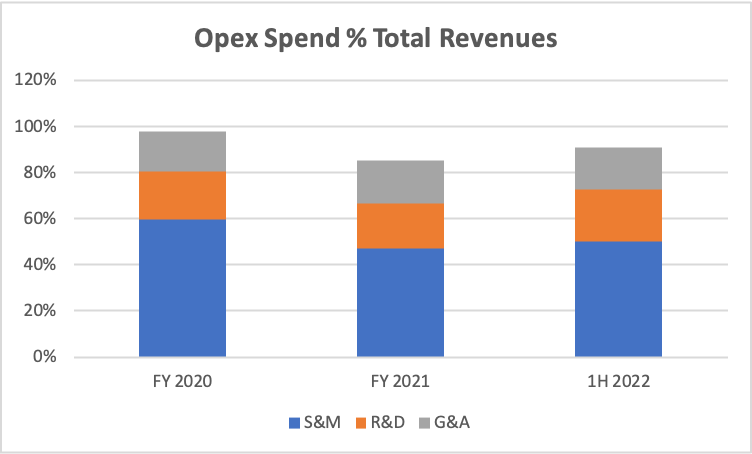

I would like to see gross margins continue to improve and for DBNRR to above 120% especially for the larger cohort of customers (ARR $500k+). Like many early stage software SaaS companies, Braze should eventually be able be more efficient at coverting sales into FCF, but the company is clearly investing for growth. Opex spend remains high. The company’s S&M spend exceeds both R&D and G&A spend. S&M spend in FY 20200 was 63% of total revenues but dropped to 47% of total revenues in FY 2021. Opex spend as a % of total revenues has consistently been over 80%:

The gross proceeds of $435.5 million from the IPO should be enough to sustain the company without needing a capital raise in the immediate future - quarterly loss for the period ending July 31, 2021 was just ($12.6 million).

At today’s valuation with a market cap of $7.6 billion and TTM sales of $186 million, the TTM P/S = 41. Given that Braze grew revenues 56% YoY in FY 2021 and 53% in 1H 2022, combined with high DBNRR and growth in customer count, it seems reasonable to assume Braze will continue posting strong revenue growth. If we assume that revenues grow 50% next year, that would put the NTM P/S ratio at 27x.

Braze exhibits a lot of characteristics that one likes to see in early stage growth companies:

Founder-led

Directors and excutive offers, as a group, own ~34% of the company

Strong revenue growth

Strong customer growth that includes well-known brands such as Etsy, Venmo and Nascar

High DBNRR for all customers and even higher for customers with ARR $500k+

Meets the Rule of 40: 1H 2021 YoY revenue growth of 53% + FCF margin of (10%) = 43%

The S-1 form quotes a study from IDC that states that the market for marketing campaign management software to reach $15.0 billion in 2021 and $19.4 billion in 2024. This is not nearly as large of a market as say cybersecurity or e-commerce, but this does not mean Braze cannot provide attractive returns for investors.

Braze is growing revenue quickly and adding customers at a nice clip. It is difficult to determine the durability of their long term growth rate at this stage. With that said, if you follow the numbers, the company is executing well as evidenced by 10 quarters of sequential QoQ growth. Braze seems to have found a product market fit as evidenced by their impressive customer list. Since the market for marketing campaign management is not experiencing hypergrowth, my sense is that Braze is likely taking market share as opposed to the popular aphorism “a rising tide lifts all boats”. The valuation seems a bit rich at the moment to invest but I am excited to see how this story unfolds.