Looking Ahead - Analyzing 2022 Macro Outlooks

I summarized 2022 market outlooks so you don't have to

TL;DR

I read some macro outlooks from major investment firms. Here are some of the common themes for 2022:

Risk assets are favorable

Consumers have excess savings that should fuel consumer demand

Earnings growth is forecasted to be good although multiple compression may hamper equity returns

Strong GDP growth forecast for 2022

Inflation pressure remains a key risk. If Fed policy results in faster than expected tightening this could be bearish for risk assets

ESG and energy transition continue to be a major investment theme

KKR states that we are currently in the mid-cycle of the post-pandemic recovery (red arrow added for emphasis):

Overview

I read the 2022 macro outlooks recently put out by three large financial firms -Northern Trust, Nuveen and KKR - to determine the consensus expecations for next year. What can investors expect? There were some similar themes across these outlooks:

Risk assets are favorable

Consumers have excess savings that should fuel consumer demand

Earnings growth forecasted to be good although multiple compression may hamper equity returns

Strong GDP growth forecast for 2022

Inflation pressure remains a key risk. If Fed policy results in faster than expected tightening this could be bearish for risk assets

ESG and energy transition continue to be a major investment theme

As of today’s writing the S&P 500 is up 23% YTD and is on track for another year of above average returns. Investors may naturally be wondering what to expect in 2022. Below I will attempt to summarize the key points behind why risk assets are generally favorable next year.

Consumers are Doing Well

Each outlook struck a bullish tone while also being cautious. Case in point look at how each firm titled their outlooks:

Northern Trust - A Transition Year

Nuveen - Slower. But still pretty fast.

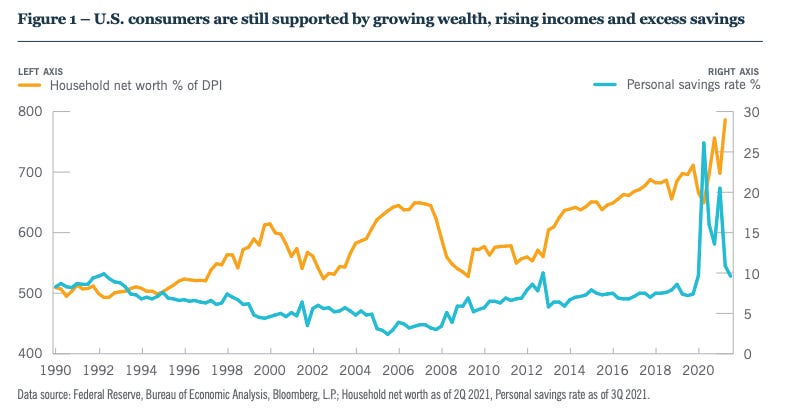

Why are these firms all favoring risk assets? One reason is that U.S. consumers are doing well. Consumers’ household net worth as a % of disposable personal income is at all time highs, incomes are rising and they have excess savings. Nuveen illustrates this with the below graph:

Northern Trust also observes that consumers in the developed world are sitting on a ‘mountain’ of excess savings. This indicates pent-up demand and will continue to support the recovery. Speaking of excess savings, KKR believes that the current macroeconomic backdrop is creating a savings bull market. Quantitative easing and the increase in disposable income has allowed consumers to save considerably more since the start of the pandemic. If it sounds odd that U.S. consumers are better off then they before the pandemic then you are not alone. KKR quotes the outgoing Fed Vice Chairman, Richard Clarida, as stating:

This was the only downturn in my professional career in which disposable income actually went up in a deep recession, and a lot of that has been saved.

‘Excess savings’, defined as a % of annual consumption spend, is expected to increase from 0% in March 2020 to 17% in December 2021:

Corporations are Doing Well Too…But Do Not Expect 2021-Like Equity Performance

All firms are expecting positive, lower equity returns compared to last year. Each firm had nearly identical statements about this:

Nuveen:

2021 provided close to ideal conditions for economic growth and risk assets like equities but we see the environment as more balanced heading into 2022.

Northern Trust:

We have a constructive outlook for 2022, but risk assets will likely fall short of 2021’s. Entering 2021 we anticipated good earnings growth but thought valuations were stretched. Lo and behold, corporate profits topped expectations…

KKR:

Importantly, while valuations and earnings are up materially versus a year ago, our base case is that we are mid-cycle for Equities mid-cycle returns are generally solid for investors, albeit they are less than early cycle ones.

Northern Trust notes that the two ‘key underpinnings’ of good stock and bond price performance are in place - strong earnings growth and low interest rates. The recovery in the stock market was fueled by earnings growth while valuation multiples declined. This trend is expected to continue in 2022. Northern Trust goes on to state that while developed market valuations should decline, lower interest rates and a global financial system flush with stimulus will help valuations stay above historical averages. The firm predicts that the S&P 500 will return 8.6% inclusive of dividends:

KKR agrees with Northern Trust equities should rise due to earnings growth and not multiple expansion. KKR is however slightly less optimistic on the S&P 500’s performance in 2022, expecting a return 6.7% inclusive of dividends:

More specifically, KKR’s base case scenario puts the S&P 500 at 4,900 at the end of 2022 on $241 in EPS

This represents a 15% increase in EPS and an 8.2% decrease in the LTM P/E from 22.1x to 20.3x. As mentioned above, Northern Trust states that valuations will stay above historical averages. JP Morgan notes in their quarterly publication Guide to the Markets that the 25-year average forward P/E for the S&P 500 is 16.78x. KKR’s 2022 base case scenario shows the forward P/E equaling 19.4x. This is is consistent with Northern Trust’s belief that valuations will stay above historical averages.

Nuveen concurs with KKR and Northern Trust that equities should rise in 2022 due to earnings growth, but differs in their view on multiple compression. Nuveen states that they expect valuations to be relatively flat.

Nuveen notes that the S&P 500 is on track for 3 consecutive years of above average returns. The S&P 500 returned 28.88% in 2019, 16.26% in 2020 and is up ~23% 2021 YTD. Additionally, KKR expects EPS growth to slow down to 15% in 2022 compared to an estimated 48% growth 2021. Given this and combined with possible multiple compression, is not too surprising that these firms are anticipating lower equity returns.

Lastly, Northern Trust states that they believe that companies should be able to maintain profit margins given excess savings and pent-up demand from consumers. KKR states that price makers, or companies whose products have few substitutes, will naturally be able to maintain profit margins in an inflationary environment. Nuveen is vautious about rising costs impacting profit margins...more on this later in the article. As of the most recent Q3 2021 data, margins are still high by historical standards at 12.3%:

GDP Growth is Expected to be Strong

All firms are expecting fairly strong GDP growth in 2022 with only slight divergence in opinions. KKR is expecting above consensus growth of 4.1% in the U.S., below consensus growth of 4.0% in Europe and below consensus growth of 4.8% for China.

Northern Trust is predicting above consensus growth in the U.S. and Europe in the range of 4-5% with China coming in at 4-6% for 2022.

Nuveen did not provide specific GDP growth target for 2022 in their report but the firm states that they “…expect global economic growth to be a notch slower than it was in 2021, but still above the long-term trend.” A notch slower likely indicates that Nuveen is likely more aligned with Northern Trust’s higher range of predictions given that the IMF projects global GDP growth to be 5.9% in 2021.

One of the possible explanations for the differences in macro outlooks is due to COVID-19. KKR’s macro outlook specifcally assumes that the Omicron variant will hinder the recovery in early 2022, but the impact will be felt in already constrained areas like travel and entertainment. Northern Trust is more optimistic while it waits on health data, noting Omicron (and other variants) should not derail global economic expansion so long as it does not lead to serious degredation in mortality, vaccine efficacy or accuracy of testing.

The “I” Word aka Inflation…2022’s Potential Red Flag

Inflation is mentioned 59 times in Northern Trust’s report, 55 times in Nuveen’s report and 74 times in KKR’s outlook. At a high level, every firm believes that inflationary pressures will continue in 2022. Northern Trust and Nuveen are a bit more optimistic about near-term inflation pressures as it relates to supply chain issues. Nothern Trust believes that inflation will be under “market” expectations in 2022, and Nuveen feels that the global goods shortage is transitory. KKR, on the other hand, believes while supply chain issues will improve, investors are too optimistic about both the degree and speed of inflation pressures easing.

Northern Trust notes that the acceleration in tapering of bond purchases is a necessary precursor to rate hikes, but warns about about premature monetary policy tightening. The majority of Fed members are currently predicting three interest rate hikes in 2022. Northern Trust importantly states that positive equity and bond returns can be realized with well telegraphed tightening cycles. Telegraphed tightenting is the key phrase here. Nuveen believes that non-telegraphed tightening, due to a tight labor market, is the biggest risk to their market outlook:

The major risk to our outlook remains a sudden tightening of financial conditions if central banks are forced to respond to inflation driven by an overly tight labor market

This graph from Nuveen indeed highlights this issue. There is demand for labor, yet there are currently more prime-age workers in the labor force than there are prime-age workers employed. In other words, more people could be working but are choosing not to work:

Speaking of a tight labor market, every firm discussed the impact of the tight labor and housing market and its impact on inflation. Northern Trust discussed that while there were signs of easing inflation pressure in some areas, strong housing and labor markets were notable areas of concern. Nuveen, also referenced in the quote above, believes that the central bank will tighten if the labor shortage continues driving wages up. KKR stated that inflationary pressure within housing and labor “remain key ares of focus”. KKR further notes how 24 of 26 headline CPI inputs are now above the Fed’s two percent long run inflation goal:

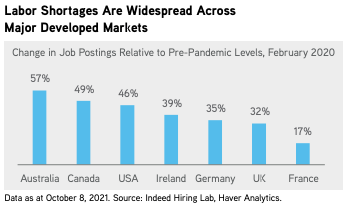

Interestingly, KKR illustrates below that labor shortages are widespread across many developed countries:

Naturally one might wonder how long the labor scarcity problem will persist. Northern Trust notes that rising wages is a natural evolution from a “winner-take-all” form of capitalism. While Northern Trust states that is unclear if the recent wage increase is temporary, change is underway as companies are currently required to pay up for scarce labor.

Outside of labor, Northern Trust is “sticking to stuckflation”. The firm believes that the recent “debt-fueled demand” will subside, automation will contain inflation, and inflation will come in lower than expectations. Future inflation will reflect the past decade rather than this past year.

Nuveen also believes that the global good shortage is transitory and inflation will slow but remain relatively high next year. Nuveen feels that inflation should not be investors’ main focus. Notably, similar to Northern Trust, Nuveen believes that long term trends will keep inflation at bay:

In the short term, interest rates are likely to creep up due to growth expectations and pandemic-related supply and demand issues. But the long-term structural impacts of demographics, technology and productivity that have kept rates low for so long are still in place.

KKR is arguably not as optimistic about inflation as Northern Trust and Nuveen. KKR believes that after four decades of disinflation we are now entering a period of reflation. Supply chain issues are easing, but not to the degree or speed that others are anticipating. Input costs will stay higher for longer. The labor shortage is a structural headwind and there will be a reconfiguration of global supply chains. Inflation is settling at a higher resting rate than in the past. There is likely too much money in the system for the current growth trajectory. KKR backs this argument by examing how much fiscal and monetary stimulus has occured this cycle versus the previous cycle in 2009:

Energy Transition is a Mega Theme

Both KKR and Nuveen consider ESG investing to be major themes. Nuveen believes climate change is the biggest issue facing society today:

There is also the potential for medium-term inflationary impetus spurred by the massive expenditures that will be required to combat climate change, currenly the world’s biggest challenge.

KKR calls ESG investment a major investment opportunity and is one of KKR’s mega themes. While KKR does not specifically mention inflation in the context of ESG investing, the firm notes that climate-related investments, especially as it relates to supply chains, “…could fuel a capex super-cycle”. This would likely lead to higher inflation. There many areas of interest with ESG investing such as renewable energy, clean technology, food sustainability. The pandemic highlighed the importance of supply chain resiliency, and Nuveen notes that supply chain management is critical to driving performance across asset classes.

KKR notes that today less than 20% of total global energy supply is linked to clean energy sources:

KKR observes that there are strategic advantages for companies pursuing ESG investments - capital markets will finance these projects more cheaply. Some companies are even shedding portions of their business to reduce their carbon foot print. Northern Trust interestingly did not discuss ESG investing in their 2022 outlook.

Conclusion

There was a fair amount of consensus around major topics. According to Northern Trust, Nuveen and KKR, one can expect a positve environment for risk assets next year, although returns will lag those achieved in 2021. There are of course risks with inflation/fed tightening being chief among them. If supply chain pressures do ease up and supply/demand equilbrium for goods is restored, then inflation concerns will be more centered around areas like housing and labor. As noted above, labor scarcity is a problem across all developed countries.

For retail investors with long term time horizons, there is likely no need to alter investment allocations. After all, economic forecasts are often wrong. This article from Mises Institute and this article from PhD economist Daniel Lacalle explain more about this phenmenon.

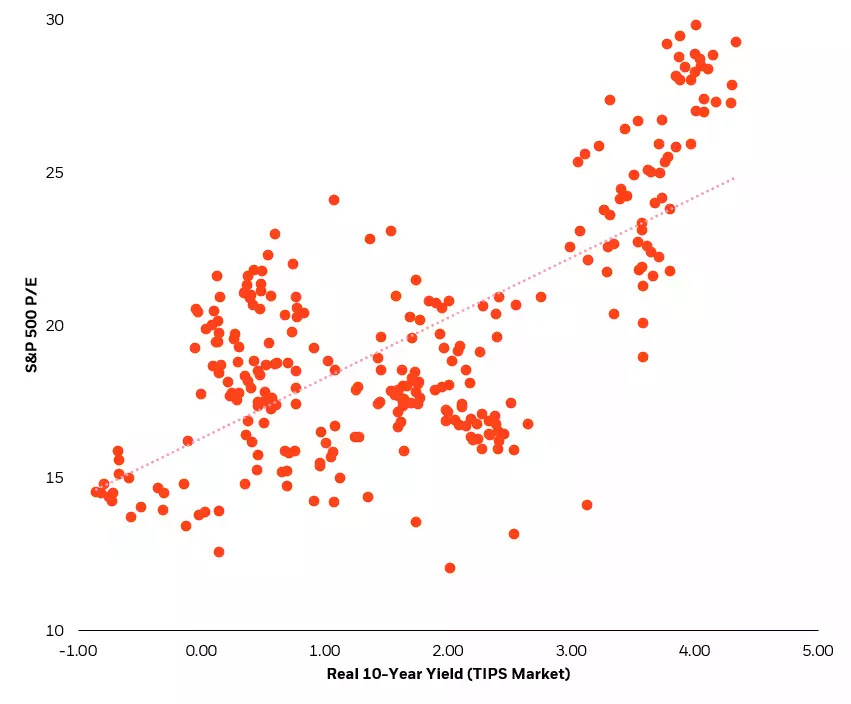

On a final note, in case you are worried about inflation or rising rates derailing stocks, Blackrock published a great article debunking this myth. History suggests that higher interest rates are actually associated with higher returns. This is because while higher rates lead to lower stock prices as future cash flows are discounted, higher interest rates are also typically accompanied by faster economic growth and earnings growth. The graph below illustrates this point. Historically higher interest rates have been associated with higher P/E multiples: